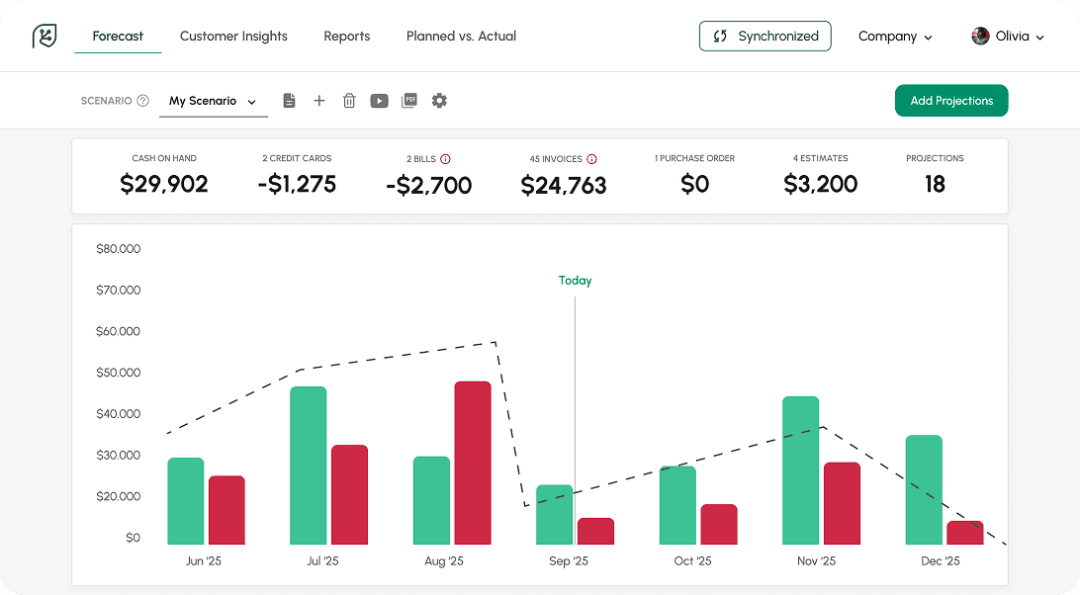

New: Setting threshold

Setting threshold

I got great news for you and for all Cash Flow Frog users. We continue to release highly requested features and here is the latest – Setting thresholds.

The new update lets you easily set thresholds. This allows you to visually monitor when your cash flow drops below a certain amount. For example, if you don’t want your cash on hand to drop below 15K, you can set up a 15K threshold that will be visible on your cash flow graph.

How it works?

Click on the cash on hand on the top left corner. Enable the Threshold toggle. Set your Threshold. That’s it.

Your threshold will always be visible on your cash flow graph.

5 Key Financial Metrics Every Business Owner Should Track

Read more

What Is Profitability Analysis and How to Do It?

Read more

Best QuickBooks Online apps

Read more

Xero Tracking Categories in Cash Flow Frog

Read more

How To Calculate Adjusted EBITDA and Why Is It So Important?

Read more

How to Calculate Profit Margin: Gross, Operating, and Net

Read more

Best cash flow forecasting software

Read more

What Is Strategic Finance, and Why Is It Important?

Read more

5 Financial Habits of Successful Entrepreneurs

Read more

Trusted by thousands of business owners

Start Free Trial Now