Cash Flow Statement: The Basics, the Format, and a Worked Example

What Is a Cash Flow Statement?

A cash flow statement is a financial report that shows how much cash entered and left a business during a specific period. Unlike the income statement, it excludes non-cash items like depreciation, so it tells you what actually hit the bank account, and where it came from.

How It's Calculated

The cash flow statement pulls from three sections, each tracking a different type of cash activity:

- Operating activities: Cash generated by running the business: customer payments received, supplier invoices paid, payroll, taxes. This is the core number most owners care about.

- Investing activities: Cash spent on or received from long-term assets: buying equipment, selling a vehicle, acquiring another business.

- Financing activities: Cash from borrowing or repaying debt, issuing equity, or paying dividends.

The formula:

Net Change in Cash = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow

That net change, added to the opening cash balance, gives you the closing cash balance, which should match what's in the bank at period-end.

There are two preparation methods. The direct method lists actual cash receipts and payments line by line. The indirect method starts with net income and adjusts for non-cash items and changes in working capital to arrive at operating cash flow.

Worked Example

Suppose a small manufacturing company closes out Q1. Here's a simplified picture:

| Section | Amount (USD) |

|---|---|

| Cash collected from customers | +$180,000 |

| Cash paid to suppliers | -$95,000 |

| Cash paid for wages | -$42,000 |

| Cash paid for taxes | -$8,000 |

| Operating Cash Flow | +$35,000 |

| Purchase of new equipment | -$20,000 |

| Investing Cash Flow | -$20,000 |

| Loan repayment | -$5,000 |

| Financing Cash Flow | -$5,000 |

| Net Change in Cash | +$10,000 |

- Opening cash balance: $40,000

- Closing cash balance: $50,000

The company is profitable and cash-positive this quarter. But notice it spent $20,000 on equipment, if that purchase hadn't happened, operating performance generated $35,000. That distinction matters when you're planning ahead.

Why It Matters in Practice

It separates profit from cash

A business can show a healthy net income while simultaneously running short on cash. That happens when revenue is recognized before it's collected, or when inventory builds up faster than sales. The cash flow statement cuts through the accrual accounting and shows the cash reality. If your income statement shows a profit but your bank balance fell, the cash flow statement explains why.

It reveals how the business funds itself

The three-section structure makes it easy to see whether cash is coming from operations (healthy) or from debt and asset sales (a pattern worth watching). A business consistently funding day-to-day expenses through loans is in a different position than one where operations generate surplus cash.

It's the starting point for any cash conversation

Lenders, investors, and accountants all look at this report first when assessing financial health. Internally, it's the document that grounds budget discussions in what actually happened rather than what was planned.

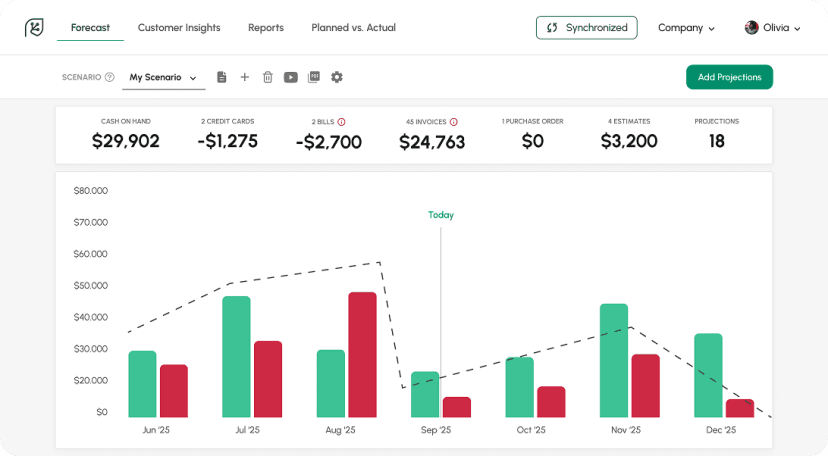

How Cash Flow Statement Affects Your Cash Flow

The statement reports cash that already moved. The forecast projects cash still to come. Read together, they show whether the trend is holding.

That distinction has real consequences. A strong operating cash flow number for the last quarter tells you the business performed well. What it doesn't tell you is whether the same conditions hold next quarter, whether that large customer will pay on the same schedule, whether the equipment purchase is done or there's more coming, whether a seasonal dip is about to compress collections. The statement is backward-looking by design. Its value as a planning tool depends on pairing it with a forward view.

When you use the statement alongside a rolling forecast, you get a clear check: does the forecast assumption match what the statement actually showed? If your projected collections came in higher than expected, that's useful calibration. If they came in lower, something in your forecast assumptions needs revisiting before you commit to spending decisions based on them.

How You'd See This in Cash Flow Frog

Cash Flow Frog connects directly to QuickBooks Online, QuickBooks Desktop, Xero, and Sage Intacct. When your accounting data syncs, the app builds a rolling forecast, up to three years out, from what your books already contain. QuickBooks records what happened. Cash Flow Frog projects what is coming.

- The practical benefit: you don't have to manually rebuild your cash position each month from the cash flow statement. The historical pattern comes in through the accounting integration, and the forecast layer sits on top of it. If you want to see why a number looks the way it does, the tool drills down to the transaction level. For businesses operating across multiple currencies or entities, that all runs natively without separate reconciliation. You can explore the forecasting features at cashflowfrog.com/features/forecast/.

Related Terms

The 3 Types of Cash Flow: What They Mean and Why They Matter

Read more

New: Setting threshold

Read more

5 Key Financial Metrics Every Business Owner Should Track

Read more

What Is Profitability Analysis and How to Do It?

Read more

Best QuickBooks Online apps

Read more

How To Calculate Adjusted EBITDA and Why Is It So Important?

Read more

FAQ

Most small businesses prepare one monthly, which matches the rhythm of their accounting close. Quarterly is the minimum if you want it to be useful for planning. Annual cash flow statements satisfy compliance requirements but offer limited practical visibility, by the time you see a problem in an annual report, it's already been a problem for months.

You can use it as a reference, but not as a forecast. The statement tells you what happened; it doesn't account for changes in payment terms, customer mix, planned capital spending, or seasonal shifts that may differ year to year. Treating historical cash flow as a straight-line projection into the future is one of the more common forecasting mistakes. The statement is an input to the forecast, not a substitute for one.

Trusted by thousands of business owners

Start Free Trial Now