10 Cash Flow Management Tips You Can Put to Work Today

Cash is easier to manage before the pressure shows up in the bank account. These cash flow management tips help you see what is available, collect money sooner, and keep payments in a sensible order. Start with today’s cash position, then work through the cash flow tips below.

Each one is built for the real work of running a business, where invoices slip, bills arrive early, customers pay late, and small costs quietly build up.

Before the Tips: Check Where Your Cash Really Stands Today

Cash flow problems often start small: an unsent invoice, a late payment, an early supplier bill, or an upcoming tax date.

Cash flow control starts with today’s position — knowing what cash is available after receipts and payments line up. The tips below build on that foundation.

Your Bank Balance Is Not the Same as Available Cash

Your bank balance shows what is in the account now, not what is already committed.

A business may have $42,000 on Monday, but payroll, sales tax, rent, suppliers, and a loan payment can shrink usable cash by Friday.

Available cash is what remains after essential payments and a minimum reserve. A key tip for managing cash flow is to ask: after payroll, tax, debt, and critical suppliers, how much is really free?

Build a One-Page Cash Snapshot

A one-page cash snapshot is enough for most weekly decisions. Keep it plain so the week is clear without a finance pack that no one updates.

- Include these items.

- Cash in the bank

- Invoices expected this week

- Overdue invoices

- Bills due this week

- Payroll

- Tax/VAT/GST

- Loan payments

- Minimum cash reserve

The snapshot separates cleared cash from expected cash and shows the shortfall, overdue amount, and bills needing action.

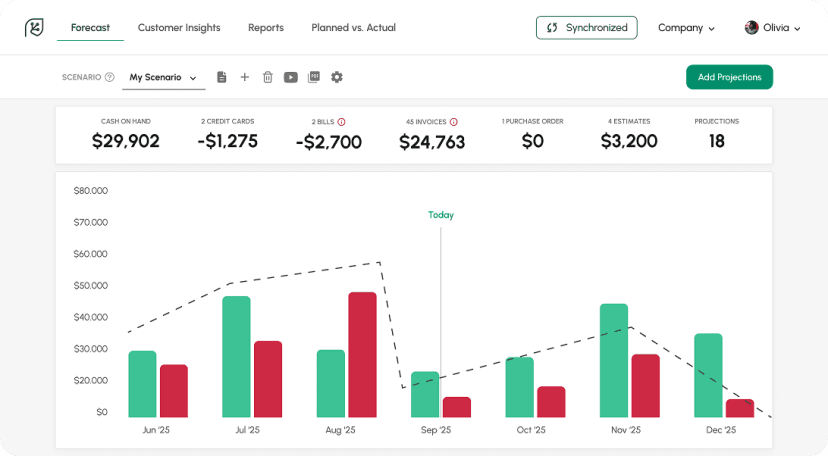

Look at the Next 13 Weeks, Not Just This Month

A monthly view can miss problems. Tax, payroll, stock orders, or supplier bills may fall before a large customer pays.

A 13-week forecast gives a better working view. It shows pressure early while the numbers are still close enough to trust.

Use it for cash flow scenario planning. Test a customer paying 10 days late, a two-week sales dip, or a supplier requesting upfront payment. Then decide what needs action now.

The next section turns this view into cash flow tips you can use today.

10 Cash Flow Management Tips You Can Implement Today

The best cash flow management tips are practical. They improve timing, reduce surprises, and support calmer payment decisions.

Each tip follows the same logic: what to do today, how it helps cash flow, and what to track.

1. Send the Invoice Before the Day Ends

What to do today

Send every ready invoice before the day ends. If the work is complete, a product has shipped, or a milestone has been approved, bill it the same day.

Why does it help cash flow? The payment clock starts when the customer receives the invoice. Waiting five days to bill adds five days to the cash gap while payroll and supplier costs keep moving.

What to track

Track completion date, invoice date, due date, and payment date. If invoices often go out late, the process is costing cash. This helps you spot delays early.

Image: Invoice on computer screen from accounting application | Shutterstock

2. Make Payment Terms Short, Clear, and Hard to Miss

What to do today

Open your latest invoice template. Check the due date, payment wording, bank details, payment link, and late payment terms. Customers should not have to search for how or when to pay.

Why does it help cash flow?

Clear terms reduce payment delays. Shorter terms will not suit every business, especially when 30-day or 60-day cycles are standard, but terms should be chosen deliberately rather than carried over by habit.

What to track

Track average days to pay and debtor days. These tips for managing cash flow can reveal weak terms, slow follow-up, or customer payment issues.

3. Make It Easier for Customers to Pay You

What to do today

Remove payment friction. Add a payment link, check bank details, and offer card, bank transfer, direct debit, or automated payment options where they fit.

Why does it help cash flow?

Customers delay when payment is hard. Missing links, unclear details, or incomplete invoices can push payment into next week.

Use milestone billing, deposits, staged payments, or instant payment links.

What to track

Track payment method, time to payment, failed payments, and invoice questions. If payment links speed up receipts, make them standard.

4. Follow Up on Overdue Invoices Before They Get Old

What to do today

Set a follow-up cadence and use it every week.

- 1 day after due date: polite reminder

- 7 days: direct follow-up

- 14 days: payment date confirmation

- 30 days: escalation or revised terms

Older invoices are more difficult to collect. Follow up while the work is still current before the invoice is buried among newer bills, forgotten, or becomes a difficult conversation after 45 days.

What to track

Track overdue value, invoice age, payment promises, and cash collected after each follow-up. Consistent tracking is one of the cash flow management techniques that keeps overdue debt visible instead of buried.

5. Know Which Customers Usually Pay Late

What to do today

Review the last six to twelve months of receipts. Sort customers by average days to pay, overdue frequency, invoice disputes, and number of reminders needed.

Why does it help cash flow?

Not all revenue behaves the same. A large, late-paying customer can put more pressure on the business than a smaller, on-time customer.

Let customer payment behavior shape your terms. Repeat late payers may need deposits, lower credit limits, staged payments, or shorter cycles.

What to track

Track average days to pay, disputes, late-payment frequency, overdue balance, and credit limit by customer.

6. Schedule Bills by Priority, Not by Panic

What to do today

List every bill due in the next two weeks. Rank each one by risk and business impact, not by who sent the sharpest reminder.

Use this order as a guide.

- Payroll

- Taxes/VAT/GST

- Critical suppliers

- Debt payments

- Non-essential subscriptions

- Discretionary spending

Why does it help cash flow

When cash is tight, the loudest demand may get paid first, but not always safely. Prioritize payroll, taxes/VAT/GST, critical suppliers, and debt before subscriptions or discretionary spending.

If a payment must be moved, contact the supplier early and, where possible, agree on a date.

What to track

Track due dates, late fees, supplier priorities, and pressure points to avoid reactive payment decisions.

7. Match Supplier Terms to Customer Payment Terms

What to do today

Compare customer payment timing with supplier payment timing. Look for gaps between cash going out and cash coming in.

Why does it help cash flow?

A profitable sale can still drain cash if costs are paid first. A 14-day supplier term and 45-day customer term create a 31-day gap.

The image shows how receivables, payables, and inventory or stock affect cash timing.

Source: Conceptual model of the study | ResearchGate

Better timing alone can ease cash pressure.

What to track

Track supplier terms, customer terms, days to pay, days to collect, gross margin, and cash tied up between delivery and receipt.

8. Cut the Quiet Costs That Drain Cash Every Month

What to do today

Review recurring payments: software, subscriptions, unused seats, duplicate tools, storage, memberships, small retainers, and services no one has reviewed recently.

Why does it help cash flow?

Quitting costs wear down cash by repeating. Do not cut everything. Some costs protect sales, delivery, customer service, compliance, security, or staff productivity.

Ask: Would we approve this again today? If not, cancel, downgrade, renegotiate, or review it. Use planned vs actual cash flow to spot overspending.

What to track

Track cost, owner, renewal date, usage, and business purpose. Every recurring cost should have someone responsible for it.

9. Stop Letting Inventory or Stock Trap Your Cash

What to do today

Review slow-moving inventory or stock. Flag items that have not sold, materials bought too early, and products that need heavy discounts to clear.

Why does it help cash flow?

Inventory or stock ties up cash until it sells, and the same applies to service firms with work in progress, prepaid materials, unused software, or unbilled project costs.

What to track

Track stock turnover, aged stock, inventory days, margins, and cash tied up in slow-moving items. These are some of the most valuable cash flow tips for product-based businesses.

10. Update Your Cash Flow Forecast Every Week

What to do today

Update the forecast with actual receipts, actual payments, changed invoice dates, new bills, payroll, tax dates, stock purchases, and customer payment updates.

Why does it help cash flow?

A forecast should not be an annual exercise. Cash changes weekly as customers pay late, suppliers shift dates, projects slip, new work starts, and tax dates get closer.

Weekly updates improve cash flow forecast accuracy and show the likely low point early, especially valuable for businesses with payroll cycles, debt repayments, seasonal sales, or project-based billing.

What to track

Track receipts, payments, forecast variance, and the 13-week low point. This keeps the forecast current.

What to Do First If Cash Is Already Tight

When cash is tight, start by finding the short-term gap, pulling cash forward, and protecting the work that keeps revenue moving.

In the First 24 Hours: Find the Short-Term Gap

Check the next seven days.

- Cash available today

- Money expected in the next 7 days

- Critical payments due in the next 7 days

- Overdue invoices

- Payments that can be delayed safely

It shows the size of the problem.

A $4,000 gap may need one overdue invoice and one delayed non-essential payment. A $40,000 gap may need customer calls, supplier talks, owner funding, credit, or tighter spending approval.

A clear number gives you better choices.

In the First Week: Pull Cash Forward Where You Can

Once the gap is known, focus on cash that can arrive sooner.

- Call the top overdue customers

- Offer partial payment options

- Invoice unbilled work

- Request deposits on new work

- Pause non-essential purchases

Call first. Ask for a payment date or partial payment.

Check unbilled work. If it is not invoiced, the admin is delaying the cash.

What Not to Cut First

Some cuts feel useful in the moment and hurt later.

Do not automatically cut these.

- Revenue-producing activities

- Customer delivery

- Compliance/tax obligations

- Critical staff

- Essential suppliers

Protect sales, delivery, compliance, key staff, and essential suppliers. Blind cuts can turn a short cash squeeze into a longer problem.

Build a Cash Flow Routine You Can Actually Stick To

Cash flow planning works best as a routine. The routine does not need to be long. It needs to be used.

Daily: Watch Cash Coming In and Going Out

Check receipts, outgoing payments, failed payments, and urgent customer money expected today. This only takes a few minutes when accounts are current.

Daily checks identify missed payments, double charges or missing receipts early. Simple, consistent monitoring is one of the most undervalued cash flow management recommendations, as it prevents little problems from snowballing.

Weekly: Review Receivables, Payables, and the Forecast

Once a week, review unpaid invoices, overdue accounts, bills due, payroll, tax, supplier payments, and the 13-week forecast.

Connect finance with operations. If a project slips, an order is placed, or a customer raises a dispute, update the forecast.

Weekly reviews are where cash flow management strategies stop being theory and become working habits.

Monthly: Compare Planned vs Actual Cash Flow

At month-end, compare the forecast with what actually happened.

Check why the gap occurred. Did customers pay late? Did supplier costs rise? Did inventory or stock purchases arrive early? Did tax or lower sales create pressure?

Use the answers to improve next month’s forecast. Good forecasting comes from repeated review, not from a single perfect model.

Source: Planned versus actual cash flow | ResearchGate

Spreadsheets, Accounting Reports, or Forecasting Software — What Should You Use?

A spreadsheet can work for a simple business, but manual errors, missing formulas, or outdated balances can distort the cash view.

Accounting reports use real transactions and show receivables, payables, revenue, expenses, and past cash movement. Many look backward, while cash flow management strategies need a forward view.

Forecasting software can help with cash flow forecasting, scenario planning, dashboards, team access, and accounting software integration.

Use the simplest tool that gives a reliable weekly view. Move beyond spreadsheets when updates take too long, errors repeat, or you need multiple forecast versions.

Small Cash Flow Habits That Matter More Than Big One-Time Fixes

Small fixes usually help you save more cash than big ones.

Invoice on time, make payments easy, monitor late accounts weekly, track days past due from customers, monitor debtors, check payment patterns from your customers, compare the terms from your suppliers and your customers, review contracts before they expire, check inventory or stock before you purchase more, and update the forecast weekly.

These cash flow management tips keep you close to the numbers and help you avoid cash emergencies.

Conclusion: Cash Flow Gets Easier When You Act Early

Cash pressure usually sends warnings: late invoices, stretched terms, stock buildup, unnoticed subscriptions, pressure-led bill payments, and forecasts that stop matching reality. Acting early gives you more room.

Build a one-page cash snapshot. Look 13 weeks ahead. Send invoices sooner. Make payment easier. Follow up on overdue accounts. Rank bills carefully. Review the quiet costs. Keep the forecast current with easy cash flow forecasting.

These cash flow management tips work because they turn cash into a regular operating habit. When the numbers are visible, decisions get easier.

The 3 Types of Cash Flow: What They Mean and Why They Matter

Read more

New: Setting threshold

Read more

5 Key Financial Metrics Every Business Owner Should Track

Read more

What Is Profitability Analysis and How to Do It?

Read more

Best QuickBooks Online apps

Read more

How To Calculate Adjusted EBITDA and Why Is It So Important?

Read more

FAQ

Invoice promptly, set clear payment terms, make paying easy, follow up early on overdue accounts, track late payers, prioritize critical bills, review recurring costs, and update a 13-week forecast weekly.

Use cash flow management strategies like sending unbilled invoices, calling overdue customers, adding payment links, pausing non-essential purchases, and listing this week’s bills.

Update the forecast weekly. It helps spot late receipts, early supplier payments, tax dates, payroll pressure, and short-term gaps before they become problems.

Starting with the money you already have. Bill your clients, get paid for your work, request deposits, and make it easy to pay.

Cut unused subscriptions, duplicate tools, and weak recurring payments. Protect anything that drives sales, supports customer delivery, or covers tax and key staff.

Many businesses aim for one to three months of operating expenses. If your revenue is uneven or you face large periodic bills, keep more.

No. Profit is what remains after expenses on paper. Cash flow is the actual money moving in and out of your account. A profitable business can still run out of cash.

When errors slip through, your team needs shared access and reliable forecasts, or updating the spreadsheet takes too long to be useful.

Trusted by thousands of business owners

Start Free Trial Now