The Prudence Concept In Accounting

Many companies lean toward optimistic financial reporting to highlight rapid growth. While it may momentarily impress stakeholders, overstating revenues or undervaluing liabilities often creates vulnerabilities. Hidden risks can surface later, damaging trust and threatening a company’s resilience.

The challenge lies in transparency. Inflated figures may boost short-term appeal, but they fail to address the uncertainties businesses face. Financial accounting requires a balance between ambition and realism, and businesses that embrace this often develop resilience over time.

The prudence concept in accounting, also known as the principle of prudence, embodies this approach. It emphasizes careful judgment, ensuring financial statements reflect a realistic view of performance and safeguard against unexpected risks.

This article explores what the prudence concept in accounting is, its applications and significance, and an overview of its benefits and challenges.

Prudence Concept Definition

The prudence concept is an accounting principle that guides companies toward conservative financial reporting. It emphasizes recognizing liabilities and expenses when they are reasonably expected while deferring the recording of revenues and assets until they are certain to be realized. This principle helps stakeholders avoid inflated financial health and promotes transparent reporting.

Prudence becomes especially significant during economic uncertainty. A study on the politics of prudence in accounting standards highlights how political and economic factors influence its application. For example, businesses may allocate provisions for bad debts or anticipated legal costs before they arise.

Similarly, uncertain revenue projections are delayed until payments are received. This ensures businesses are prepared for risks and fosters confidence among stakeholders.

In essence, the prudence principle in accounting:

- Encourages early recognition of liabilities and expenses while deferring revenues and assets until certain.

- Prevents overstated profits and understated liabilities, ensuring accuracy.

- Builds trust by presenting transparent and reliable financial data.

- Helps account for potential risks during economic challenges.

- Promotes disciplined financial practices and long-term resilience.

What is the Prudence Concept?

So, what is prudence in accounting? The prudence concept impacts how companies decide when to record revenues and expenses. These decisions significantly affect the transparency and accuracy of financial reporting.

Recognized Revenues

Under the prudence principle, revenues are recorded only when their realization is certain. For example, a company delivering goods on credit to a financially unstable customer would delay recording revenue until payment is received.

This practice aligns with the principle of substance over form, ensuring that financial reporting reflects actual business outcomes rather than contractual optimism. It reduces the risk of misleading stakeholders by inflating profits prematurely.

Recognised Expenses

Expenses, on the other hand, are recognized as soon as there is a reasonable expectation they will occur, even if the cash outflow happens later. For instance, a car manufacturer anticipating warranty claims would record a provision for repair costs based on historical data, even before repairs are requested.

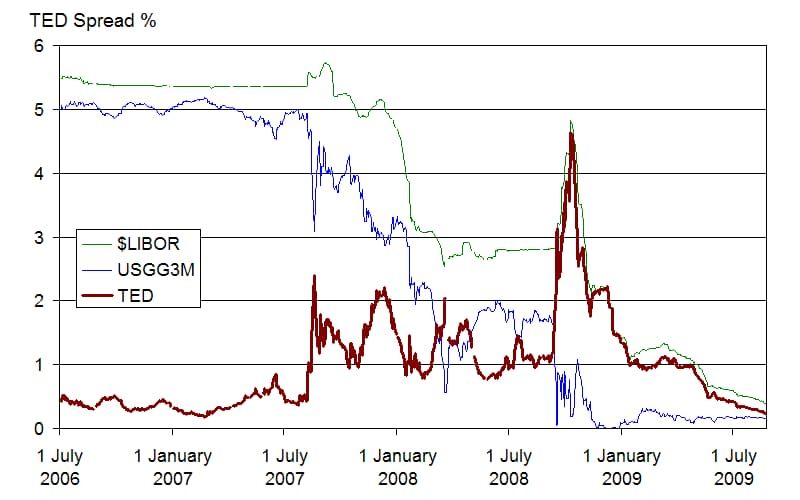

Case in Point: To better understand what the prudence concept is, consider the 2008 financial crisis. The soaring TED spread, a key credit risk indicator, exposed the fragile trust among financial institutions.

Image: TED spread (in red) and components during the financial crisis of 2007–08 | Wikipedia

Many companies failed to account for potential loan defaults, leading to unexpected losses and financial instability. Companies adhering to the prudence concept were better equipped to handle the crisis, having accounted for risks early and maintained stability.

Uses and Importance of Prudence Concept in Accounting

The prudence concept of accounting ensures financial statements are transparent, risk-aware, and compliant with regulatory standards, strengthening trust and credibility.

Building Stakeholder Confidence

The meaning of prudence accounting emphasizes avoiding over-optimistic projections to provide a realistic view of financial health. Recognizing liabilities early and only recording assured revenues ensures stakeholders have reliable data to base decisions on, fostering long-term confidence.

Managing Risks

By addressing uncertainties early, such as setting aside reserves for bad debts, businesses mitigate financial shocks and protect liquidity. Prudence equips companies to handle disruptions, fostering stability during volatile periods.

Ensuring Compliance

Prudence aligns with key international accounting frameworks like the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). Adhering to these standards prevents compliance issues and enhances credibility in global markets.

Image: NicoElNino | Shutterstock

Pros and Cons of Prudence Concept

Like any accounting principle, the prudence concept has its strengths and limitations. Understanding both is essential to applying the principle effectively.

Pros of Prudence Concept

The principle of prudence in accounting provides several key advantages, particularly in promoting financial accuracy and trustworthiness.

1. Prevention of Financial Overstatements

One of the most significant advantages of prudence is its ability to curb inflated financial statements. By requiring businesses to recognize liabilities and expenses early while deferring uncertain revenues, prudence ensures profits are not overstated and obligations are accurately represented.

2. Support for Long-Term Planning

Companies are encouraged by prudence to foresee risks and provide financial buffers. Companies that prepare for potential economic downturns are better equipped to handle market turbulence and preserve operational stability, which will eventually guarantee sustained development.

3. Alignment with Stakeholder Interests

Transparent and conservative reporting aligns with the interests of investors, regulators, and creditors. Stakeholders value financial statements that prioritize accuracy over optimism, especially during volatile economic periods when trust in a company’s stability is essential.

Cons of Prudence's Concept

While the prudence concept strengthens financial discipline, it also introduces potential challenges that businesses must navigate carefully.

1. Overly Conservative Estimates

Excessive conservatism can result in undervaluing assets or understating profits, potentially discouraging investors and portraying an unnecessarily pessimistic financial position.

2. Reliance on Subjective Judgment

The application of prudence often involves estimating future liabilities or revenues, which can vary significantly depending on the accountant's perspective. For example, two accountants might interpret the likelihood of a lawsuit’s outcome differently, leading to inconsistencies in reporting.

3. Complexity in Application

Identifying and estimating probable future liabilities or revenues requires thorough analysis and expertise. For example, accurately predicting warranty costs or loan defaults involves detailed historical data and predictive modeling, which can complicate the financial reporting process.

Examples of Prudence's Concept in Accounting

Various accounting scenarios provide examples of the prudence concept and its impact on financial decision-making.

Inventory Valuation

Inventory is valued at the lower of cost or net realizable value (NRV) under the prudence principle of accounting. If the market value falls below cost, the lower figure is recorded to reflect potential losses.

Example: A retailer purchases 1,000 units of a product at a cost of $50 per unit. Later on, the market value drops to $45 per unit.

- Cost: 1,000 units × $50 = $50,000

- NRV: 1,000 units × $45 = $45,000

The inventory is recorded at $45,000 due to the NRV being lower than the cost. This avoids overstatement of assets and provides a realistic picture of potential losses. Such conservative valuation protects stakeholders by recognizing potential losses early rather than overstating the company’s financial health.

Provision for Bad Debts

Prudence also applies when estimating uncollectible accounts receivable. This makes sure that possible losses from clients who don't pay are planned for beforehand.

As an illustration, a company has $200,000 in unpaid accounts receivable. The business projects that 5% of its receivables will be uncollectible based on historical performance predictions.

- Estimated Bad Debts: $200,000 × 5% = $10,000

This $10,000 is recorded as an expense in the current period, reducing net income. Such precaution allows recognition of potential losses in advance, thereby avoiding sudden financial shocks and providing a clearer view of liquidity.

Contingent Liabilities

The prudence principle also guides how potential obligations, like lawsuits, are reported. If there’s a high probability of losing a case and the costs can be estimated, the liability is recognized.

Example: With an estimated $500,000 in damages, a corporation has a 70% chance of losing a case.

The company's income statement shows a $500,000 cost, but its balance sheet shows a $500,000 contingent obligation.

If the likelihood were below 50%, the liability wouldn't be recorded but disclosed in financial statements.

A Commitment to Responsible Reporting

By focusing on careful judgment and modest estimations, the prudence principle guarantees accurate, trustworthy financial reporting. Because it gives companies the tools to make wise decisions, boosts stakeholder trust, and guarantees adherence to financial reporting requirements, putting this idea into practice is strategically essential.

For organizations seeking to align their financial practices with this principle, adopting advanced tools like Cash Flow Frog's forecasting software can make a significant difference. Embrace technology to simplify complex processes while aligning with the prudence concept to safeguard your financial future.

How to Calculate Free Cash Flow (FCF): Formulas + Real Examples

Read more

The 3 Types of Cash Flow: What They Mean and Why They Matter

Read more

Cash Flow Forecasting Template

Read more

Your Guide To Financial Metrics And KPIs

Read more

10 Cash Management Trends for 2026

Read more

10 Best Cash Flow Business Ideas: Build Income That Counts

Read more

FAQ

Trusted by thousands of business owners

Start Free Trial Now