What is the Cash Flow Gap?

What Is a Cash Flow Gap?

A cash flow gap is a period when a business's outflows exceed its inflows, causing the bank balance to fall short of what is needed to meet obligations. The business may be profitable and growing, the gap is about timing, not necessarily performance.

How It's Identified

There is no single formula for a cash flow gap, but it is measured by projecting the running cash balance forward and identifying periods where it falls below zero or below a minimum operating threshold:

Projected Closing Balance = Opening Balance + Projected Inflows - Projected Outflows

When the projected closing balance for any period is negative, or below whatever minimum the business needs to operate, that period contains a cash flow gap. The size of the gap is the difference between the projected balance and the required minimum. The duration is how many consecutive periods the shortfall persists.

What drives gaps varies. Common causes are:

Receivables lag, customers pay on longer terms than suppliers require, so the business is always funding a timing difference between buying and collecting.

Seasonal demand, revenue concentrates in certain months while costs run throughout the year, creating recurring troughs at predictable points in the calendar.

Growth investment, hiring, inventory buildup, or capital expenditure consumes cash before the associated revenue arrives.

Lumpy large payments, a tax bill, an insurance renewal, or a large supplier invoice falls in the same period as lower-than-usual inflows.

Identifying the cause matters because it changes the response. A structural receivables gap requires a different fix from a one-time tax payment coinciding with a slow collections month.

Worked Example

A wholesaler has a reliable order book but extended customer payment terms. It is projecting its cash position over six weeks. Opening balance: $42,000.

WeekInflows (USD)Outflows (USD)Net (USD)Closing Balance (USD)Week 1+$28,000-$31,000-$3,000$39,000Week 2+$19,000-$24,000-$5,000$34,000Week 3+$14,000-$38,000-$24,000$10,000Week 4+$11,000-$22,000-$11,000-$1,000Week 5+$34,000-$18,000+$16,000$15,000Week 6+$41,000-$19,000+$22,000$37,000

The gap appears in Week 4, where the closing balance goes negative by $1,000. The business returns to positive by Week 5 when a batch of customer payments arrives. The gap is narrow and short, but without seeing it in advance, the business would not know to act until the payment was already due and the account was short.

With four weeks of warning, the options are manageable: accelerate collection on one outstanding invoice, draw briefly on a credit facility, or negotiate a short deferral on the Week 3 or Week 4 outflows. None of those conversations is difficult four weeks out. They are very difficult on the day.

Why It Matters in Practice

Gaps are predictable if you look forward

Most cash flow gaps do not appear without warning. The information that creates them, an invoice due date, a payroll schedule, a supplier payment term, is already in the business's books before the gap materialises. The gap is invisible only when no one is looking ahead. A business projecting its cash position weekly or monthly will see the gap forming in the data well before it arrives in the account. One that only reviews the bank statement after the fact will see it when there is nothing left to do.

Timing is the difference between a manageable problem and a crisis

The same cash shortfall has very different consequences depending on how much notice the business has. Four weeks of lead time means lenders will talk, suppliers may negotiate, and customers can be asked to pay earlier. Four days of lead time means emergency calls, penalty interest on late payments, and the reputational cost of bouncing a supplier payment. The gap itself is the same size in both cases. The outcome is not.

Gaps recur at recognisable points for most businesses

Businesses with predictable payment cycles, seasonal patterns, or regular large outflows tend to see their cash flow gaps appear at the same points each year. Tax quarters, payroll cycles, and seasonal troughs are not surprises, they are scheduled. A business that has been through a few annual cycles can anticipate when its gaps typically arrive and build that knowledge into its cash planning, rather than treating each one as a fresh emergency.

How Cash Flow Gap Affects Your Cash Flow

A cash flow gap is a period where outflows beat inflows. Spotting it weeks ahead turns a crisis into a calm financing decision.

The shift from crisis to decision is entirely a function of time. When the forecast shows a negative closing balance in Week 4, that week is still four weeks away. The business has time to evaluate its options with clear numbers in front of it: how large is the gap, how long does it last, and what is the least costly way to cover it. That might mean accelerating one receivable, drawing on a credit line for a week, or simply moving a discretionary outflow by ten days. None of those options requires urgency to execute when there is lead time behind them.

What the forecast also shows is the shape of the gap, not just that the balance goes negative, but how it gets there and how it recovers. In the example above, the gap is driven by a concentration of outflows in Weeks 3 and 4 against lighter inflows, followed by a recovery in Week 5. Knowing the recovery is coming means the business does not need a permanent solution, a short bridge is sufficient. A business without forecast visibility might respond to the same gap with a larger or longer financing decision than the situation actually requires, because it cannot see when the inflows resume.

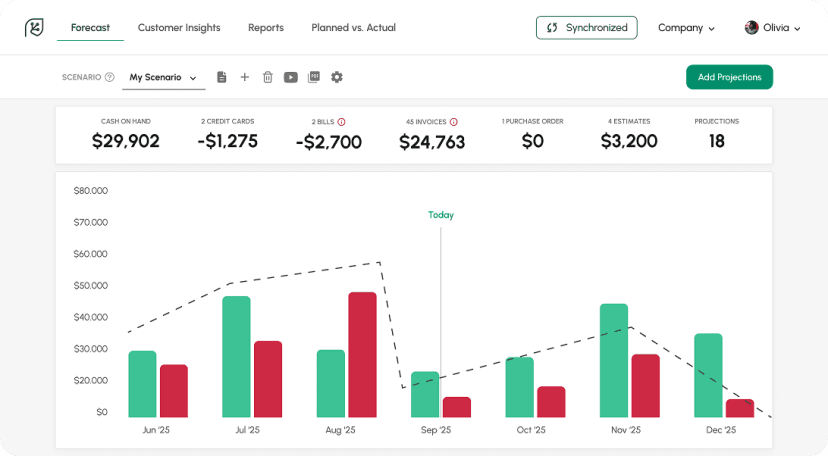

How You'd See This in Cash Flow Frog

Cash Flow Frog connects to QuickBooks Online, QuickBooks Desktop, Xero, and Sage Intacct and builds a rolling cash flow forecast automatically from your accounting data. QuickBooks records what happened. Cash Flow Frog projects what is coming.

Because the forecast pulls from live accounting data, actual outstanding invoices, scheduled bills, known payroll, it shows the projected bank balance as it moves forward in time, including any periods where it falls short. You can drill down to the transaction level to see exactly which inflows and outflows are creating a gap in a specific week, which makes the decision about how to respond much more precise than a summary figure allows. For businesses with multiple entities or currencies, that view runs natively across all of them, up to three years out. You can explore the forecasting features at cashflowfrog.com/features/forecast/.

Related Terms

New: Setting threshold

Read more

5 Key Financial Metrics Every Business Owner Should Track

Read more

What Is Profitability Analysis and How to Do It?

Read more

Best QuickBooks Online apps

Read more

How To Calculate Adjusted EBITDA and Why Is It So Important?

Read more

Best cash flow forecasting software

Read more

FAQ

Trusted by thousands of business owners

Start Free Trial Now