Current Liabilities: Meaning, Examples, and How to Calculate Them

What are current liabilities? They’re the short-term bills a business has to pay within the next year, and they end up shaping far more day-to-day decisions than most people expect. Even businesses that look healthy can feel tight on cash when these obligations stack up. They affect how much money is actually available, how careful spending needs to be, and how much flexibility the business really has. When they’re clearly understood, planning feels realistic. When they aren’t, cash pressure builds quickly.

Definition: What Are Current Liabilities?

The definition of current liabilities is obligations a business expects to pay within its normal operating cycle or within 1 year, whichever comes first. These are not rare or unusual items. They come from simply running the business.

Put more plainly, the meaning of current liabilities is what your business already owes in the short term. This often includes unpaid supplier invoices, wages employees have already earned, taxes due soon, and loan repayments scheduled for the coming months. The formal definition of current liabilities is based on timing, not importance. An obligation is considered current if it is due soon.

Understanding what are current liabilities are in business helps fix a common misunderstanding. A strong bank balance can look comforting, but it does not tell you what that money is already reserved for. Current liabilities explain that gap.

Current vs Non-Current Liabilities

Financial reports on a laptop - Image | Pexels

Not all liabilities place the same level of pressure on a business, which is why accounting separates short-term obligations from those that can be paid over a longer period. Understanding this difference helps businesses prioritize payments and plan cash flow more realistically.

What are Current and Non-Current Liabilities?

Every business obligation falls into one of two buckets based on timing. Current liabilities are due soon. Non-current liabilities are later owing, often spread over several years.

Both show up as balance sheet liabilities, but they answer very different questions. Current liabilities tell you what needs attention now. Non-current liabilities show long-term commitments such as multi-year loans or leases. Knowing what current and non-current liabilities are keeps short-term pressure from getting mixed up with long-term planning.

Key Differences in Timing and Risk

The difference that matters most is urgency. Current liabilities do not wait. They often need to be paid whether customers have paid you yet or not. That timing mismatch is where stress usually starts.

Non-current liabilities tend to follow predictable schedules. Current liabilities directly affect working capital and are usually the first place problems show up. When people talk about cash being tight, short-term obligations are almost always involved.

Common Types of Current Liabilities

Knowing the types of current liabilities shows where short-term pressure actually comes from. Cash issues usually aren’t random. When you break those liabilities down, it’s easier to see which payments are routine, which depend on timing, and which could turn into a problem. That makes it easier to decide what to pay first and avoid getting caught off guard.

Accounts Payable

Accounts payable are amounts owed to suppliers for goods or services already received. For most businesses, this is the most frequent short-term obligation.

Think of inventory delivered today with payment due in thirty days. Even if the inventory sells immediately, the bill still has to be paid. Tracking accounts payable closely helps avoid late fees and uncomfortable supplier conversations.

Short-Term Loans & Credit Lines

Short-term loans and lines of credit that must be repaid within a year are often used to bridge gaps between expenses and incoming payments.

They can help temporarily, but they also lock in repayments. If revenue slows, those payments do not. Without visibility, short-term liabilities can quietly add pressure rather than ease it.

Accrued Expenses

Accrued expenses are costs that have already been incurred but not yet paid. Common examples include wages, utilities, interest, and professional fees.

Payroll is a familiar example. Employees may have worked several days by the month-end that will not be paid until the next payroll run. Those wages still count as obligations, even if the payment happens later.

Taxes Payable

Paying taxes - Image | Pexels

Taxes payable include income tax, payroll tax, and sales tax owed to authorities. These obligations usually have firm deadlines and little flexibility.

Sales tax often confuses. The cash may sit in your account, but it does not belong to the business. Until it is paid, it remains a liability that needs to be planned for.

Unearned Revenue

Unearned revenue occurs when customers pay in advance for goods or services that have not yet been delivered. Until delivery, the business still has value.

This can feel misleading. Cash comes in, and the account balance looks strong, but the obligation remains. Treating unearned revenue correctly prevents a false sense of financial comfort.

Current Portion of Long-Term Debt

When a loan spans several years, the portion due within the next twelve months is treated as a current liability.

This makes upcoming repayments visible in short-term planning instead of hiding them inside long-term totals.

How Do You Calculate Current Liabilities?

Knowing how to calculate current liabilities takes a lot of uncertainty out of short-term planning. The process itself is simple. List every obligation that must be paid within the next year and add them together.

The current liabilities formula usually includes accounts payable, short-term loans, accrued expenses, taxes payable, unearned revenue, and the current portion of long-term debt. You may also see this called the formula for current liabilities in accounting references.

A consistent current liabilities calculation helps ensure decisions are based on what is actually owed, not what you hope is owed.

Impact on Short-Term Liquidity

Current liabilities matter because they represent cash that will leave the business soon. They are compared against assets that can quickly be turned into cash to understand flexibility.

Metrics like the current ratio and quick ratio rely on accurate numbers. When obligations rise faster than liquid assets, pressure builds even if sales look steady.

Predicting Upcoming Payments

When current obligations are clearly tracked, upcoming payments are easier to forecast, reducing the risk of surprises. You know what is coming and roughly when it will be due.

That clarity changes behavior, making spending decisions more deliberate and reducing the number of choices made under pressure.

How Forecasting Tools Reduce Financial Blind Spots

Forecasting tools and cash flow software connect cash flow and liabilities into a forward-looking view. Instead of relying solely on past reports, they show how future payments align with expected inflows and outflows. This visibility gives businesses time to adjust spending, delay decisions, or build buffers before tight periods turn into real problems.

If tracking current liabilities still feels scattered, using a dedicated tool can help bring everything into focus. Cash Flow Frog connects upcoming obligations with expected cash movements in one clear view, making planning easier and more reliable. Sign up to see how better visibility can support more confident financial decisions.

Current Liabilities on Financial Statements

You’ll find current liabilities on the balance sheet, grouped under liabilities and usually ordered by how soon they’re due. That setup makes it easier to see what needs to be dealt with first and where short-term pressure is building.

The problem is that a balance sheet only shows a snapshot of one moment in time. Bills get logged, payments go out, and costs change, so real cash rarely moves exactly as planned. What looks fine on paper can drift quickly once timing shifts.

That’s where tools like Cash Flow Frog come in. By comparing planned cash flow with what actually happened, businesses can see where assumptions missed the mark. Looking at those gaps regularly helps tighten forecasts, stay on top of short-term obligations, and make planning feel a lot less like guesswork.

Current Liabilities Examples

Clear current liabilities examples help turn the concept into something practical. A retail business may list unpaid supplier invoices, wages owed at month-end, and sales tax collected but not yet paid in its internal reports. Seeing these items together makes it easier to understand how much cash is already committed.

A service business may track accrued fees for completed work, advance payments from clients, and outstanding expenses. These examples show how obligations can exist even when cash is on hand. Using the same current liabilities examples consistently across reports helps identify patterns and improve short-term planning.

How to Manage and Reduce Current Liabilities

Managing short-term obligations isn’t about dodging bills. It’s about knowing what’s coming and being ready for it. Cash pressure usually shows up when payments hit before money comes in, or when too many bills land at the same time. Things get easier once the timing is clear and nothing is a surprise.

Negotiating better payment terms can spread obligations more evenly, especially with long-term suppliers. Aligning customer billing with payroll and supplier schedules helps cash arrive before it needs to go out.

Limiting short-term borrowing reduces fixed repayments that can quickly tighten cash, while consistent expense tracking ensures no obligation is missed.

When current liabilities are planned for instead of handled at the last minute, they become predictable rather than stressful. This shift makes cash management steadier and day-to-day decisions easier to make.

Current Liabilities in Small vs Large Businesses

Small businesses feel current liabilities more than most because there’s usually less room to absorb mistakes. Cash cushions are thinner, payments don’t always come in on time, and a single delay can start to ripple into payroll, supplier bills, or taxes.

Larger businesses usually have steadier inflows and stronger systems, but they also manage much larger sums. Even small timing mismatches can create pressure at scale. In both cases, clear visibility into upcoming obligations matters, which is why cash flow forecasting is essential regardless of business size.

When that visibility is built into everyday planning, managing current liabilities becomes far more practical. Cash Flow Frog is designed to support this kind of day-to-day clarity by focusing on upcoming payments and expected inflows, helping businesses stay ahead of short-term obligations as they grow. Explore Cash Flow Frog for businesses to see how clearer cash visibility can support steadier decisions.

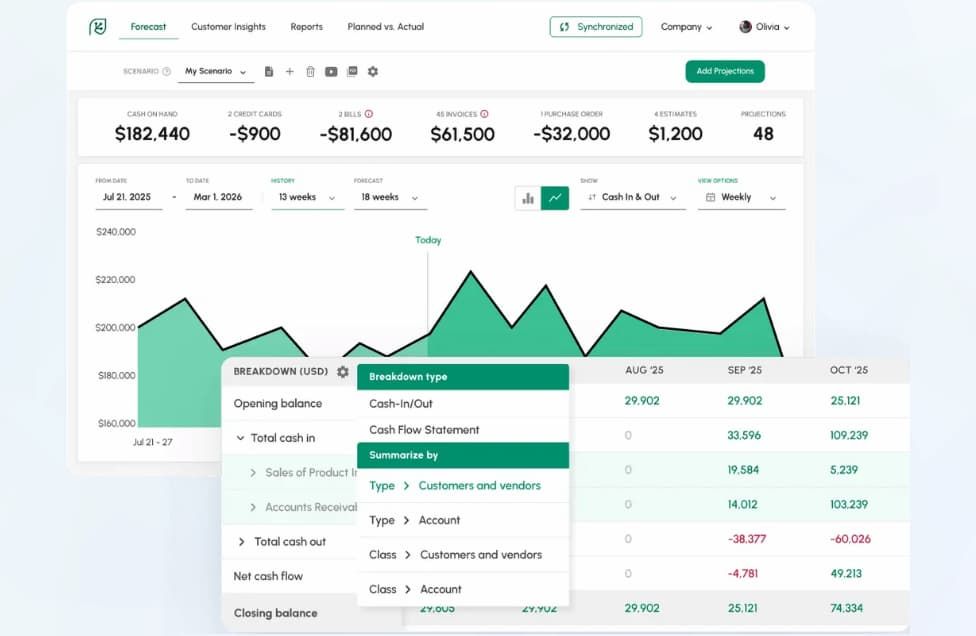

Want a Clear View of Your Current Liabilities? Try Cash Flow Frog

Cash Flow Frog interface - Image | Cash Flow Frog

Clarity changes how businesses behave. When current liabilities are scattered across reports, it becomes hard to see how today’s decisions affect cash later.

Cash Flow Frog brings current liabilities into a forward-looking cash view by linking upcoming payments with expected inflows. This makes tight periods easier to spot early and gives businesses time to adjust.

With a clearer picture of how cash and obligations interact, planning feels steadier and less reactive.

The 3 Types of Cash Flow: What They Mean and Why They Matter

Read more

What Is a Finance Charge? A Simple Explanation You’ll Actually Use

Read more

Current Assets Explained: Meaning, Types, and How They Work

Read more

Cash Flow Forecasting Template

Read more

Your Guide To Financial Metrics And KPIs

Read more

10 Cash Management Trends for 2026

Read more

FAQ

Trusted by thousands of business owners

Start Free Trial Now